The Headlines Say Exit. The Math Says Trim.

Why ₹4 lakh crore of FII selling looks scary in a headline and ordinary in a spreadsheet.

One number. Two interpretations. Only one of them is honest.

You have probably read this somewhere in the last few weeks: “FIIs have sold ₹4 lakh crore worth of Indian equities in 2025 and 2026 combined.”

It is true. And on the surface, it sounds alarming.

But here is the question almost nobody asks: ₹4 lakh crore is big compared to what?

Because a number alone is meaningless. Context is everything. So let me show you the same number in proper perspective.

Three numbers. One conclusion.

One. FIIs sold ₹4 lakh crore.

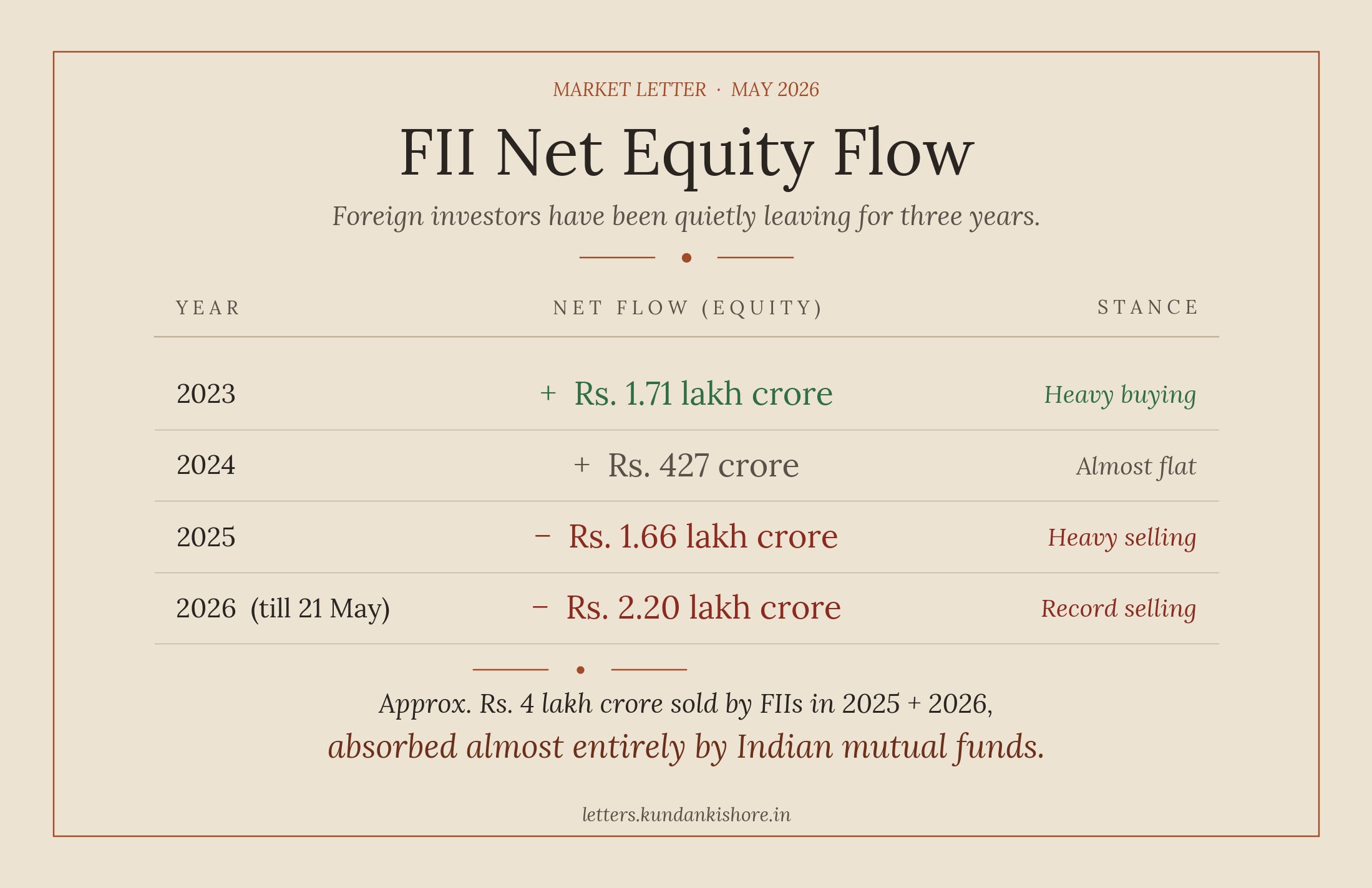

Across 2025 and 2026 year-to-date, foreign investors net sold approximately ₹4 lakh crore worth of Indian equities. This is a real number, and it is the largest two-year outflow in the recent history of Indian markets.

Two. FIIs still hold ₹74 lakh crore.

Despite all the selling, foreign investors still own roughly 16% of India’s total market capitalisation, which is approximately ₹74 lakh crore of Indian companies. They have not exited India. They have not abandoned the story. They still have more skin in the Indian game than almost any other investor category outside our own mutual funds.

Three. ₹4 lakh crore is just ~1.7% of free float.

Now here is where most retail investors get the math wrong. India’s total market cap of ₹461 lakh crore is misleading because most of it is locked away with promoters, government, and long-term strategic holders. The shares that actually trade every day, the free float, is only about ₹200 to 230 lakh crore.

Against that free float, ₹4 lakh crore of selling is about 1.7%. Less than two paise out of every rupee that genuinely moves in the market.

What this really means.

FIIs have trimmed about 5% of their India position over two years. They have not run for the exit. They have rebalanced.

Why? Three boring reasons.

The dollar got stronger and the rupee weakened from around 85 to 96. Their USD returns from India got worse, so some money went back home.

US markets, especially AI-driven names, looked irresistible. Money chases the best risk-adjusted return.

Indian valuations were rich at the top, so some profit booking was natural.

None of these reasons are “India is collapsing.” None of them are permanent.

The headlines say exit. The math says trim.

How the selling unfolded.

To really understand the shift, look at the three-year trajectory, not just the headline of 2026.

In 2023, FIIs were heavy buyers. In 2024, they essentially stopped buying. In 2025 they turned net sellers, and in 2026 the pace accelerated. So the shift is real and it is structural, not a one-month panic.

But notice something important. Every rupee they sold has been absorbed by Indian mutual funds, by your SIPs, by domestic money. For the first time in our history, the floor under Indian equities is not set by foreigners. It is set by us.

So why does the market feel so heavy then?

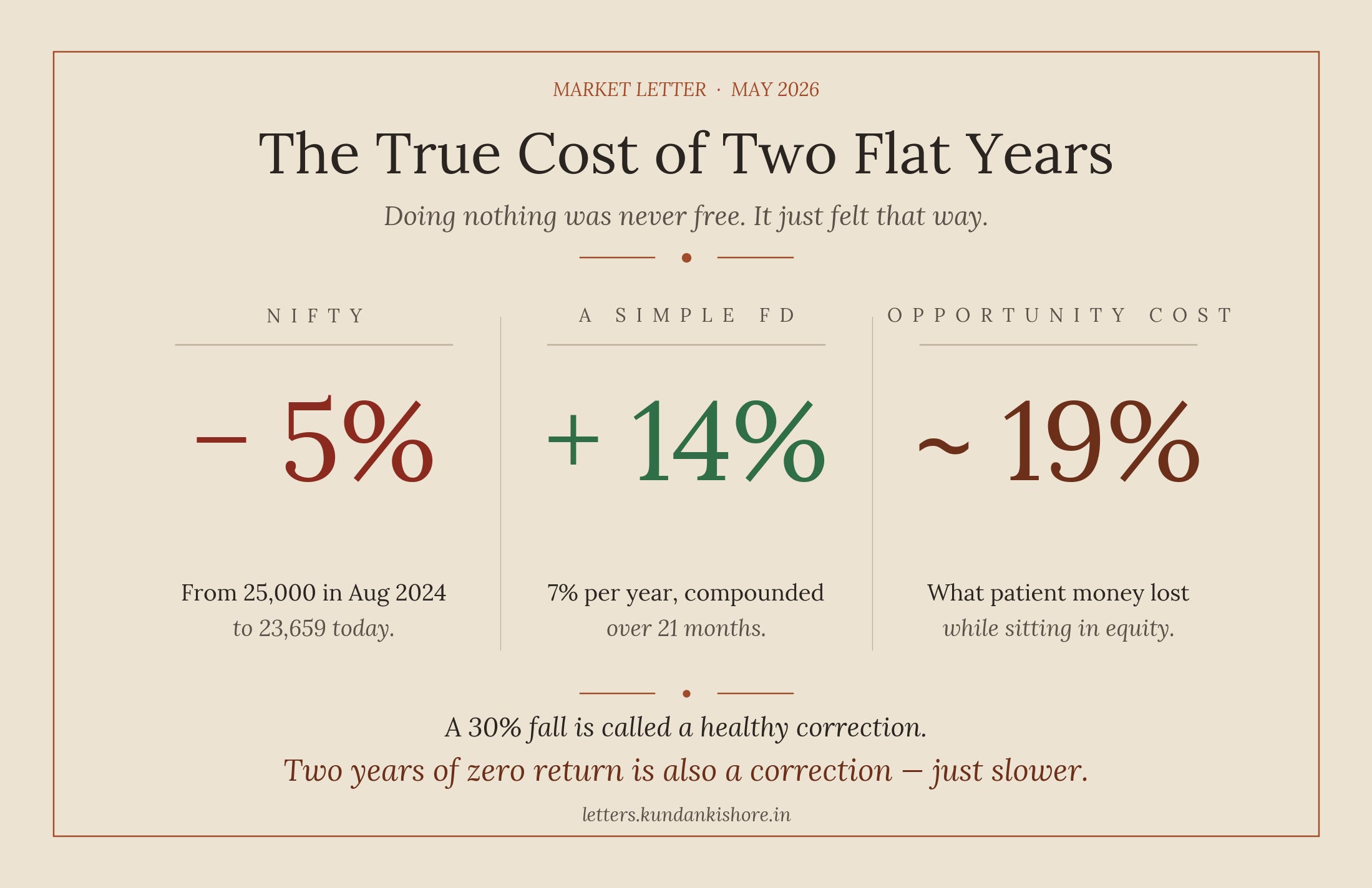

Good question. If the selling is only 1.7% of free float, why has Nifty given almost no returns for nearly two years?

The reason is simple. FIIs are price-setters, not just shareholders. They set the marginal price in large-cap stocks. When they sell HDFC Bank, Reliance, or Infosys, there is no equivalent natural buyer at the same price. DIIs buy, but at lower prices. That is how 1.7% of selling drags the index 10%.

This is not a flaw. It is just how price discovery works at the margin in any market.

The hidden cost most investors miss.

Here is something nobody talks about. Two years of zero returns is not really zero.

If your money had been sitting in a simple FD earning 7% per year, it would have compounded to around 14% over this same period. So an equity investor who stayed put has effectively lost close to 19% in opportunity cost, even if the absolute number on the screen looks only slightly negative.

In market language, a 30% fall from the top is called a healthy correction. Two years of zero return is also a correction, just a slower and more painful one.

This is actually good news. It means we are not at the top anymore. We are somewhere in the middle of a correction that has already done a lot of its work.

So what should you do?

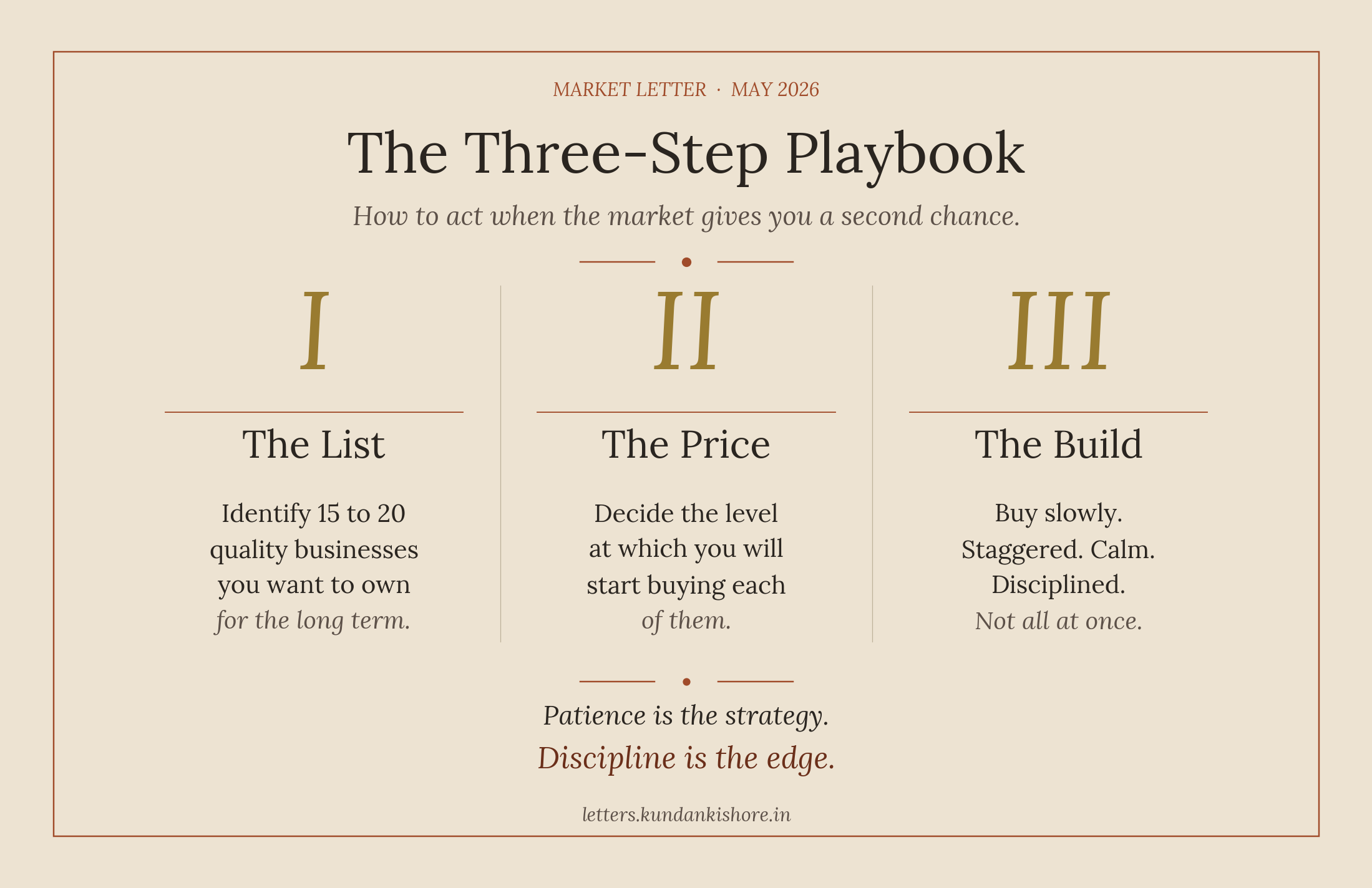

Three simple steps, the kind I have shared with my students for years.

Make a list of 15 to 20 quality stocks you want to own for the long term.

Decide a target price for each, the level at which you will start buying.

Build your portfolio slowly. Staggered, calm, disciplined. Not all at once.

The next 6 to 12 months are likely to give patient investors a chance to buy quality businesses at reasonable prices. But remember, not all stocks will bottom out at the same time. Some will fall earlier, some later.

A final word on India.

Yes, the rupee is weak. Yes, FIIs have been net sellers for two years. Yes, GDP numbers have some genuine credibility issues we can debate another day.

But India still has the demographics, the domestic consumption base, the digital infrastructure, and the savings culture that very few large economies have today.

Things are uncomfortable. They are not catastrophic.

Being cautious is better than being careless. But being permanently negative on our own country’s growth story is neither correct nor helpful, not for our portfolios, and not for our nation.

Stay calm. Stay invested. Stay learning.

Kundan Sir, your article clarifies an important query in my mind: is FII behaviour overhyped? Most of the media houses are only sensationalizing issues rather than throwing light on them . Your view made it clear. Thank you.

have you considered the impact of income slowdown in a phase when FIIs are net sellers. Net of outstanding forward, India has 8 months of import cover. So in a situation, that oil fall back to $60-65/ bl and the supply gets upto 80-90% normalcy, can we anticipate minimum impact of war on income levels and inflation. otherwise rationing of fuel and other steps are demand and growth negative. Parallely, sustained high oil prices are inflationary over medium term as it shows its second round impact. this could spiral into earnings of indian corporate and act as another trigger for FIIs to continue their selling spree. Which is why it is way too early to brush off impact of west war as a passe. the broad macros are extremely important at this stage.